The year 2026 brings significant shifts in tax regulations, especially concerning how we handle our assets after we’re gone. Understanding the differences between inheritance tax and estate tax is crucial for anyone planning their financial future or assisting in estate settlement. These taxes can impact beneficiaries and the estate itself, making it vital to grasp the nuances of each.

This overview will clarify the core distinctions between inheritance and estate taxes, highlighting who pays what, when, and how. We’ll explore state-specific variations, planning strategies, and the impact of federal laws. Whether you’re a financial planner, a potential beneficiary, or simply curious, this guide will provide a clear understanding of these complex tax issues.

2026 Tax Update: Inheritance Tax vs. Estate Tax Differences by State

Navigating the world of inheritance and estate taxes can feel like traversing a complex maze. In 2026, understanding the nuances of these taxes is crucial for anyone looking to plan their financial future or manage an estate. This article delves into the core differences between inheritance and estate taxes, explores state-specific variations, and provides practical insights to help you navigate these potentially challenging waters.

Let’s break down the key elements to provide clarity and empower you with the knowledge you need.

This article will explain the key differences, state-specific variations, and planning strategies for inheritance and estate taxes in 2026. It’s designed to provide a clear, easy-to-understand guide for individuals, families, and anyone interested in financial planning.

Understanding the Fundamental Distinctions Between Inheritance and Estate Taxes in the Year 2026

The core differences between inheritance and estate taxes are significant and impact how assets are handled after someone passes away. Estate taxes are levied on the value of the deceased person’s estate before it’s distributed to beneficiaries. This means the tax is paid directly from the estate itself, reducing the total amount available for distribution. The estate, therefore, is responsible for the tax liability.

Inheritance taxes, on the other hand, are levied on the beneficiary. The tax is calculated based on the amount each individual inherits and their relationship to the deceased. This means the beneficiaries, not the estate, are responsible for paying the tax. This distinction has important implications for both the estate and the beneficiaries, affecting the financial burden and the planning strategies that are most effective.

The triggers for these taxes also differ. Estate tax is triggered when the total value of the deceased person’s assets exceeds a certain threshold, set by the federal government and, in some cases, individual states. This threshold is often substantial, meaning that smaller estates may not be subject to the tax. Inheritance tax, however, is triggered when an individual inherits assets from a deceased person residing in a state that levies this tax.

The trigger is the act of inheritance itself, and the tax liability is determined by the value of the inherited assets and the relationship between the beneficiary and the deceased. Some jurisdictions have exemptions for certain types of beneficiaries, such as spouses or direct descendants, further complicating the landscape.

For example, imagine a scenario where a person dies in a state with an estate tax. If the estate’s value exceeds the state’s exemption amount, the estate must pay estate taxes before the assets are distributed. Conversely, if a person dies in a state with an inheritance tax, the beneficiaries will be responsible for paying taxes on the amounts they inherit.

The tax rate often depends on the beneficiary’s relationship to the deceased; a spouse might pay no tax, while a distant relative might pay a higher rate. These varying triggers and responsibilities highlight the importance of understanding the specific tax laws of your state and the implications for your beneficiaries.

To further illustrate the differences, consider this table:

| Tax Type | Taxpayer | Tax Base | Applicable Thresholds |

|---|---|---|---|

| Inheritance Tax | Beneficiary | Value of inherited assets | Thresholds vary by state, often based on the relationship to the deceased. |

| Estate Tax | Estate | Total value of the deceased’s assets | Federal and state thresholds apply; Federal in 2026: $13.61 million (per individual). |

Examining State-Specific Variations in Inheritance Tax Structures in 2026

The landscape of inheritance taxes in the United States is not uniform. Several states impose inheritance taxes, each with its own set of rules, rates, and exemptions. In 2026, the specific tax rates, exemptions, and thresholds can vary significantly, creating a complex web for estate planning. Understanding these state-specific nuances is crucial for both residents and those with assets in these jurisdictions.

The relationship between the deceased and the beneficiary plays a significant role in determining the inheritance tax burden. Many states offer exemptions or lower tax rates for close relatives, such as spouses, children, and parents. More distant relatives, such as siblings, nieces, nephews, or unrelated individuals, often face higher tax rates and fewer exemptions. This tiered system is designed to recognize and support family relationships, with the tax burden increasing as the relationship becomes more distant.

For example, consider a hypothetical state with an inheritance tax. If a person leaves their entire estate to their spouse, the inheritance may be entirely exempt from tax. However, if the same person leaves the estate to a sibling, the sibling may be subject to a tax rate that varies depending on the value of the inheritance. If the inheritance goes to an unrelated individual, the tax rate could be even higher.

This illustrates the importance of understanding the specific rules of the state in which the deceased resided and the potential tax implications for different beneficiaries.

Here are some potential planning strategies to minimize inheritance tax liabilities:

- Trusts: Using trusts, such as irrevocable life insurance trusts (ILITs) or qualified personal residence trusts (QPRTs), can remove assets from the taxable estate, thereby reducing the inheritance tax burden. However, these can be complex and require careful planning.

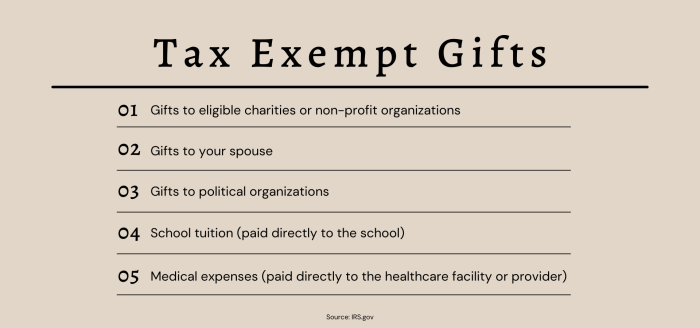

- Gifts: Making annual gifts to beneficiaries can reduce the size of the taxable estate. The annual gift tax exclusion allows individuals to gift a certain amount each year without incurring gift tax. This is simple, but limits the amount that can be gifted.

- Life Insurance: Life insurance policies can be used to provide funds to cover inheritance tax liabilities, ensuring beneficiaries receive the intended inheritance. However, the policy must be structured carefully to avoid estate tax implications.

- Charitable Giving: Donating to qualified charities can reduce the taxable estate. This benefits both the estate and the chosen charity.

Exploring State-Specific Variations in Estate Tax Structures in 2026

While the federal government levies an estate tax, several states also impose their own estate taxes. The specific tax rates, exemption amounts, and how these differ from federal estate tax regulations create a complex landscape. These state-level estate taxes can significantly impact the financial impact on estates, particularly in states with lower exemption thresholds.

Estate tax thresholds vary significantly from state to state, impacting estates of varying sizes. The federal estate tax exemption is typically much higher than many state thresholds. This means that an estate might not be subject to federal estate tax but could still be liable for state estate taxes. The difference in exemption amounts can lead to considerable tax burdens, especially for estates in states with lower thresholds.

For example, imagine an estate valued at $8 million. In a state with an estate tax exemption of $5 million, the estate would be subject to state estate tax on $3 million. However, if the same estate were located in a state with an exemption of $10 million, no state estate tax would be due. This illustrates how state-specific thresholds can dramatically affect the amount of tax owed and the overall distribution of assets.

Here is a step-by-step procedure outlining the process of filing an estate tax return in a hypothetical state (note: actual procedures vary by state):

- Determine if a Return is Required: Verify if the estate’s gross value exceeds the state’s exemption threshold.

- Obtain an EIN: Apply for an Employer Identification Number (EIN) from the IRS for the estate.

- Gather Assets and Liabilities: Compile a complete inventory of all assets (real estate, investments, etc.) and liabilities (debts, mortgages).

- Complete the State Estate Tax Return: Fill out the required state forms, which often mirror the federal estate tax return (Form 706).

- Calculate Tax Due: Calculate the taxable estate and the amount of tax owed, using the state’s tax rates.

- File the Return and Pay Taxes: File the return with the state’s tax authority and pay the tax due by the deadline.

- Gather Supporting Documentation: Include appraisals, bank statements, and other relevant documents to support the values reported.

Navigating the Complexities of Tax Planning for Both Inheritance and Estate Taxes in 2026

Effective tax planning is crucial to minimize both inheritance and estate tax liabilities. Several strategies can be employed, often involving the strategic use of financial instruments and legal structures. Careful planning ensures that assets are distributed according to the deceased’s wishes while minimizing the tax burden on beneficiaries.

Tax planning strategies to minimize both inheritance and estate tax liabilities include:

- Trusts: Trusts, particularly irrevocable trusts, can be used to remove assets from the taxable estate.

- Life Insurance: Life insurance policies can provide funds to cover estate taxes.

- Gifts: Gifting assets during one’s lifetime can reduce the size of the taxable estate.

- Charitable Giving: Donating to qualified charities can reduce the taxable estate.

Each approach has its advantages and disadvantages. Gifting strategies, for example, allow individuals to reduce their taxable estate during their lifetime but may involve gift tax implications. The use of irrevocable life insurance trusts (ILITs) can protect life insurance proceeds from estate taxes, but the setup can be complex and require ongoing management. Careful consideration of these trade-offs is essential to develop an effective tax plan.

Potential pitfalls to avoid when planning for inheritance and estate taxes include:

- Inadequate Documentation: Failing to maintain accurate records of assets, liabilities, and gifts.

- Failure to Update Estate Plans: Not reviewing and updating estate plans regularly to reflect changes in tax laws and personal circumstances.

- Insufficient Professional Guidance: Not seeking advice from qualified attorneys, CPAs, and financial advisors.

Analyzing the Impact of Federal Tax Laws on State Inheritance and Estate Taxes in 2026

Federal tax laws significantly influence state inheritance and estate tax regulations. The federal estate tax, for example, often serves as a baseline, with states either mirroring federal regulations or setting their own, potentially more stringent, rules. Changes in federal tax laws can have a ripple effect, impacting state tax revenues and estate planning strategies.

Changes in federal tax laws can significantly impact state tax revenues and estate planning strategies. For example, if the federal estate tax exemption increases, states that base their estate tax on the federal framework might see a decrease in the number of estates subject to state tax. This can lead to a reduction in state tax revenues. Conversely, if federal tax laws become more favorable to taxpayers, states might adjust their laws to capture a larger share of estate tax revenue.

Here is a hypothetical scenario:

Suppose federal tax reform lowers the federal estate tax exemption significantly. This change would likely increase the number of estates subject to federal estate tax. In response, a state that currently has an estate tax exemption lower than the federal level might consider lowering its own exemption to capture more tax revenue. This could result in higher estate tax liabilities for estates in that state, requiring individuals to revisit their estate planning strategies.

Addressing the Role of Professional Advice in Inheritance and Estate Tax Planning for 2026

Navigating inheritance and estate tax planning requires expert guidance. Seeking professional advice from attorneys, certified public accountants (CPAs), and financial advisors is crucial. These professionals can provide valuable insights, ensure compliance with tax laws, and help individuals develop effective estate plans.

When selecting an estate planning professional, ask these questions:

- What is your experience in estate planning, and what are your qualifications?

- What are your fees, and how are they structured?

- What is your area of expertise, and do you specialize in estate and inheritance tax planning?

- How often will you review and update my estate plan?

- Can you provide references from other clients?

Consider this scene: The client, Sarah, sits across from her financial advisor, David, in his well-lit office. Sunlight streams through large windows, offering a view of the city. The office is modern and comfortable, with bookshelves lining one wall. David leans forward, gesturing towards a detailed chart outlining inheritance and estate tax planning strategies. Sarah’s expression is focused, with a slight furrow in her brow as she considers the implications of various financial instruments.

The discussion centers on the use of trusts and life insurance, with David explaining the advantages and disadvantages of each. The meeting reflects a proactive approach to financial planning, ensuring that Sarah’s assets are managed effectively and that her beneficiaries are protected from unnecessary tax burdens.

Final Thoughts

In conclusion, navigating the 2026 tax landscape requires careful consideration of both inheritance and estate taxes. From state-specific rates to federal influences, informed planning is essential. By understanding the key differences, potential strategies, and the importance of professional advice, individuals can better protect their assets and ensure their wishes are honored. Staying informed is the best way to navigate these complexities effectively.

Top FAQs

What’s the main difference between inheritance and estate tax?

Estate tax is levied on the total value of the deceased’s estate before distribution, while inheritance tax is levied on the beneficiaries who receive the assets.

Which states have inheritance taxes in 2026?

As of now, the specific states imposing inheritance taxes in 2026 can vary, so it’s essential to check the latest updates, but traditionally they include states like Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania.

How do I find out the estate tax threshold in my state?

Estate tax thresholds vary significantly by state. You can find this information by checking your state’s Department of Revenue website or consulting with a tax professional.

What are some common strategies to minimize estate taxes?

Common strategies include gifting assets during your lifetime, using trusts, and purchasing life insurance. Professional advice is crucial for determining the best approach.

When should I seek professional advice regarding estate planning?

It’s advisable to seek professional advice as early as possible, especially if you have significant assets, complex family situations, or are concerned about tax implications. This includes consulting with attorneys, CPAs, and financial advisors.